The Math of Ruin: Why the Empire Toppled

The fall of the Jaypee Group is a cautionary tale of extreme over-leverage in capital-intensive industries. The journey began with Jaiprakash Gaur, a diploma engineer who transformed from a "hill contractor" into a titan of Indian infrastructure.

"A diploma engineer from Roorkee who started in 1958 as a 'hill contractor' with just ₹10,000, Gaur built the 'Temples of Modern India,' including the massive Tehri and Sardar Sarovar dams."

In years 2004-2005 Jaypee ventured into real estate with a large expanse of 1162 acres on the Noida Expressway, probably a first amongst the whole Delhi-NCR property market.

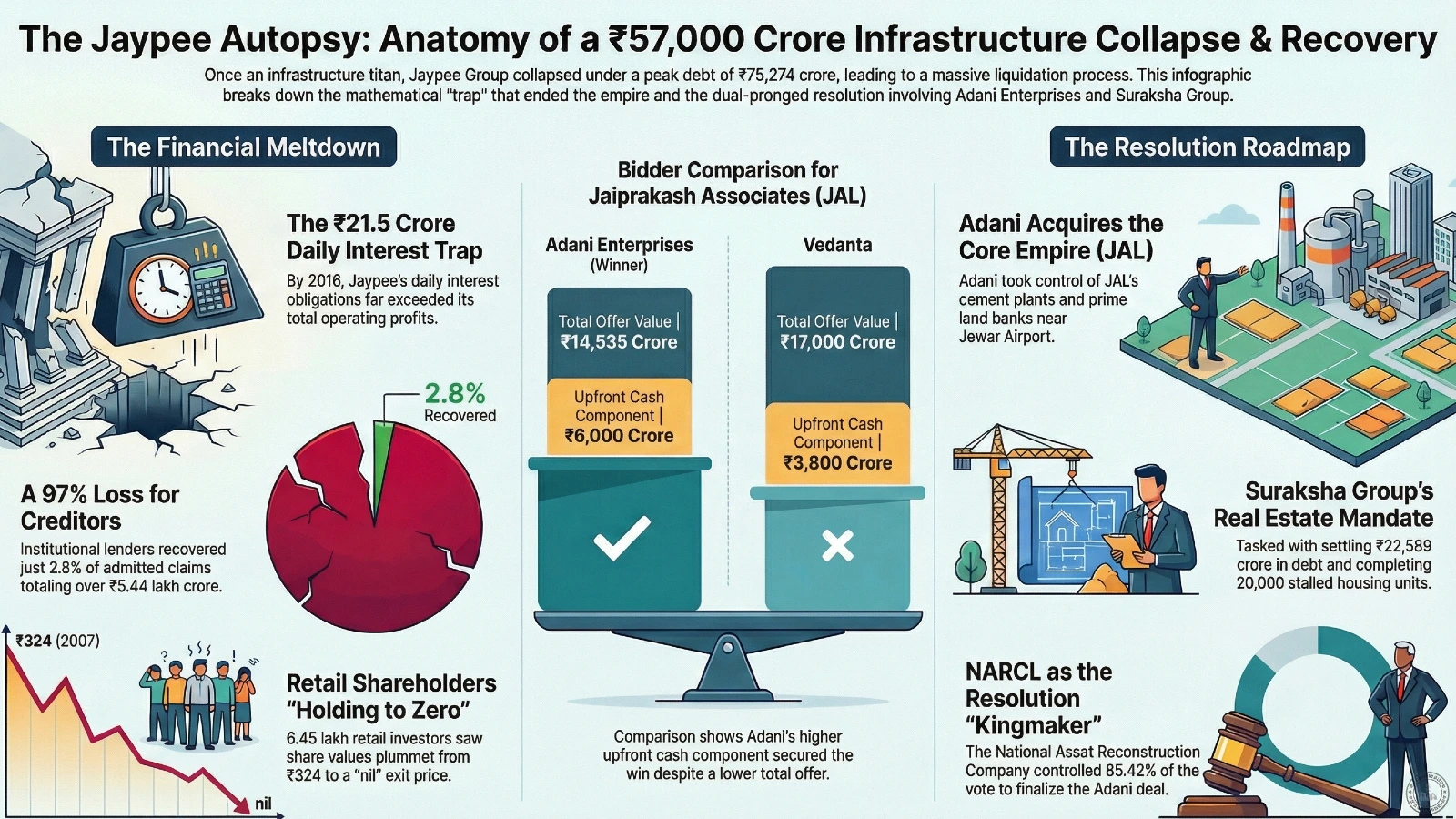

However, the transition from building dams to managing a multi-sector conglomerate was fueled by a catastrophic debt load. By March 2015, the group’s consolidated borrowings peaked at ₹75,274 crore. Jaypee built a house of cards by borrowing heavily for hydropower, expressways, and cement projects simultaneously—long before these assets could generate the cash flow required to service the debt.

The ₹21.5 Crore Daily Interest Trap By the 2016 fiscal year, Jaiprakash Associates Limited (JAL) faced an annual interest bill of ₹7,847 crore. This meant the company owed its lenders approximately ₹21.5 crore in interest every single day. With an operating profit of only ₹4,871 crore that same year, the company was racking up debt faster than a Formula 1 car. The eventual crash was a mathematical certainty.

--------------------------------------------------------------------------------

Takeaway 1: Adani’s Strategic Entry into the JAL Empire

After a grueling process of vetting and bidding, Adani Enterprises Ltd emerged as the Successful Resolution Applicant (SRA). Adani’s final plan, submitted on October 14, 2025, and clarified on November 5, 2025, was not merely a financial rescue; it was a calculated move to leverage JAL’s massive cement and logistics interests. Adani’s plan is ultimately a bet on how India’s infrastructure and Noida micro-markets will behave over the next decade.

The acquisition passed through rigorous regulatory checkpoints, including critical Competition Commission of India (CCI) approval received on August 26, 2025, ensuring the deal met anti-trust standards before the final vote.

The Committee of Creditors (CoC) favored the Adani proposal with a decisive 93.81% majority, signaling a new era of operational stability for the assets once held by the Gaur family.

Adani vs. Vedanta: Why "Cash on the Table" Won the Day

When the Committee of Creditors (CoC) finally moved to resolve JAL’s ₹57,497 crore in admitted financial debt, a high-stakes bidding war erupted between Adani Enterprises and Vedanta. While the headline figures seemed to favor one side, the banks prioritized immediate liquidity and Net Present Value (NPV) over long-term promises.

Vedanta’s Bid: Offered a higher total value of ₹17,000 crore, but included only ₹3,800 crore in upfront cash, with the remainder staggered over five years.

Adani’s Bid: Offered a lower total value of approximately ₹14,535 crore, but provided a much larger ₹6,000 crore in upfront cash.

By choosing Adani, the banks effectively left ₹2,500 crore on the table to avoid "execution risk." For lenders trapped in a stress cycle for fifteen years, a five-year payout plan was a wager they were no longer willing to take. For retail buyers tracking Noida property investment, this kind of over-leverage explains why some projects turned into decade-long delays.

--------------------------------------------------------------------------------

Takeaway 2: The Staggering Scale of Debt (₹57,497 Crores)

The sheer financial gravity of the JAL insolvency is highlighted by the gap between claimed and admitted amounts. While the total claims reached astronomical heights, the Resolution Professional (RP) meticulously verified and admitted ₹57,497.93 Crore.

To illustrate the concentration of exposure and the "haircuts" involved, consider the top three financial creditors from the 27-member CoC:

National Asset Reconstruction Company Limited (NARCL): ₹49,119.06 Cr (Admitted) / ₹49,589.83 Cr (Claimed)

Asset Care & Reconstruction Enterprise Limited: ₹2,314.90 Cr (Admitted)

Axis Bank Limited: ₹911.69 Cr (Admitted)

Beyond these institutional figures lies the human cost: the RP admitted claims for 21,256 Home Buyers (totaling ₹2,125.67 Cr), whose lives remained in limbo for years as the conglomerate's real estate projects stalled. For many of these buyers, the basic question today is whether Noida is still a good place to buy property after such turbulence.

--------------------------------------------------------------------------------

Takeaway 3: The "Challenge Process"—A 5-Round High-Stakes Bidding War

To ensure "transparency in negotiations" and "maximize the value of assets," the CoC implemented a unique "Challenge Process" on September 5, 2025. This was a high-pressure, five-round digital auction where participants submitted password-protected Excel bids evaluated on Net Present Value (NPV).

While six entities initially submitted plans—including Dalmia Cement and Vedanta—only Adani and Vedanta ultimately stepped into the ring for the final challenge rounds. The rules were designed to prevent the tactical backsliding often seen in large-scale defaults:

"The financial proposals submitted during the Challenge Process shall be unconditional and irrevocable and cannot be modified in any manner whatsoever subsequent to the Challenge Process."

This mechanism forced bidders to put their "best and final" numbers on the table, ensuring the CoC could exercise its commercial wisdom with absolute clarity.

--------------------------------------------------------------------------------

Takeaway 4: NARCL—The Kingmaker of the Resolution

The consolidation of debt was the strategic masterstroke that broke the deadlock. On March 11, 2025, a Deed of Assignment was executed, transferring significant debt from various banks to the National Asset Reconstruction Company Limited (NARCL).

By November 5, 2025, NARCL commanded a massive 85.42% voting share in the CoC. Because the IBC requires a 66% majority for plan approval, the other 26 members were essentially powerless against NARCL's preference. As the "Kingmaker," NARCL’s alignment with the Adani proposal was the single most critical factor in crossing the finish line.

--------------------------------------------------------------------------------

Takeaway 5: Keeping it Whole—The Defeat of the "Cluster" Strategy

A major point of contention was whether to sell JAL as a single entity (Option I) or carve it up into business verticals like cement and real estate (Option II). The latter "Cluster-wise" strategy was seen by some as a way to attract specialized bidders, but it threatened the "going concern" status of the parent company.

The legal death knell for the cluster strategy came via a Tribunal order on March 6, 2025, which set aside Option II. This forced the RP to proceed with the EOI for the Corporate Debtor as a whole, protecting the integrity of the resolution and ensuring that the eventual SRA would take responsibility for the entire sprawling enterprise rather than cherry-picking assets.

--------------------------------------------------------------------------------

Takeaway 6: The Last-Minute 12A Drama

In a move typical of a failing dynasty, the original promoters attempted a "tactical disruption" in the final hours. On October 4, 2025, suspended director Mr. Manoj Gaur submitted a proposal under Section 12A of the Code to regain control of the company.

However, the resolution process had already moved into a phase of deep due diligence. The RP had even engaged Kroll Associates (India) Pvt Limited to conduct rigorous Section 29A eligibility checks to ensure no errant promoters or ineligible parties could subvert the process. The 12A attempt was ultimately sidelined by the overwhelming commercial momentum of the Adani bid.

--------------------------------------------------------------------------------

The Suraksha Factor: A Different Battle for Homebuyers

It is vital to distinguish between Jaiprakash Associates Ltd (JAL) and its subsidiary, Jaypee Infratech Ltd (JIL). While Adani dismantles the parent (JAL), the Suraksha Group is tasked with the residential rescue of JIL, the entity behind Jaypee Wish Town.

Suraksha took operational control in June 2024 with a mandate to complete 20,000 stalled units. However, the path to completion is mired in controversy, another reason why new buyers today prefer ready-to-move flats in Noida instead of betting on long-horizon construction risk.

Reported Progress: Suraksha claims to have completed 5,989 flats by early 2026.

The ₹230 Crore Legal Alert: In January 2026, the Delhi Police registered an FIR against Suraksha Group, alleging the diversion of ₹230 crore meant for construction into associated entities like ITI Gold Loans.

Oversight: Due to intense homebuyer skepticism and delays, the NCLT has appointed a two-member committee to independently assess progress and grievances. For families waiting since 2010, the psychological toll is immense, with many not expecting possession until 2029.

--------------------------------------------------------------------------------

The Retail Investor’s "Ghost Ship"

While institutional lenders are salvaging what they can, the 6.45 lakh retail shareholders of JAL are facing a total wipeout. Many bought into the company when it was an infrastructure darling trading at ₹324 per share.

Today, that stock price is a hallucination. The insolvency disclosures reveal a "nil" exit price for existing shareholders. As part of the resolution, the shares will be cancelled and the company delisted. This highlights a brutal disconnect in the Indian insolvency system: while banks use the CoC to mitigate losses, small-time savers are left on a "ghost ship," holding paper that the legal system has declared worthless.

--------------------------------------------------------------------------------

Conclusion: A Landmark for Indian Insolvency

The final order, pronounced on March 17, 2026, marks the end of a grueling nearly two-year CIRP. For the 21,256 homebuyers and thousands of employees, this resolution provides a definitive path forward under one of India’s most well-capitalized groups.

From an analyst’s perspective, the JAL case is a triumph of debt consolidation and structured bidding. While the timeline was long and the debt mountain staggering, the successful deployment of the "Challenge Process" and the role of NARCL as a centralizing force sets a new benchmark for resolving mega-conglomerates. The question now is whether the Indian banking system can prevent such ₹57,000 crore fortresses from being built in the first place, or if the IBC remains the only pincer strong enough to breach them. Cases like JAL will shape bank behaviour and real estate trends for 2026 far beyond one conglomerate.