The Jaypee Group fund diversion case revolves around explosive allegations that the promoters of Jaiprakash Associates Ltd (JAL) and Jaiprakash Infratech Ltd (JIL) systematically siphoned off nearly 95% of the money collected from homebuyers.

Instead of deploying these funds to construct the massive residential projects across Noida, Greater Noida, and the Yamuna Expressway (like the sprawling Jaypee Greens), the money was funneled into separate group companies and third-party real estate entities, leaving over 25,000 homebuyers stranded for over a decade, similar echoes the diversion patterns of other real estate developers, whether it is Supertech Supernova or the Parsvnath group insolvency.

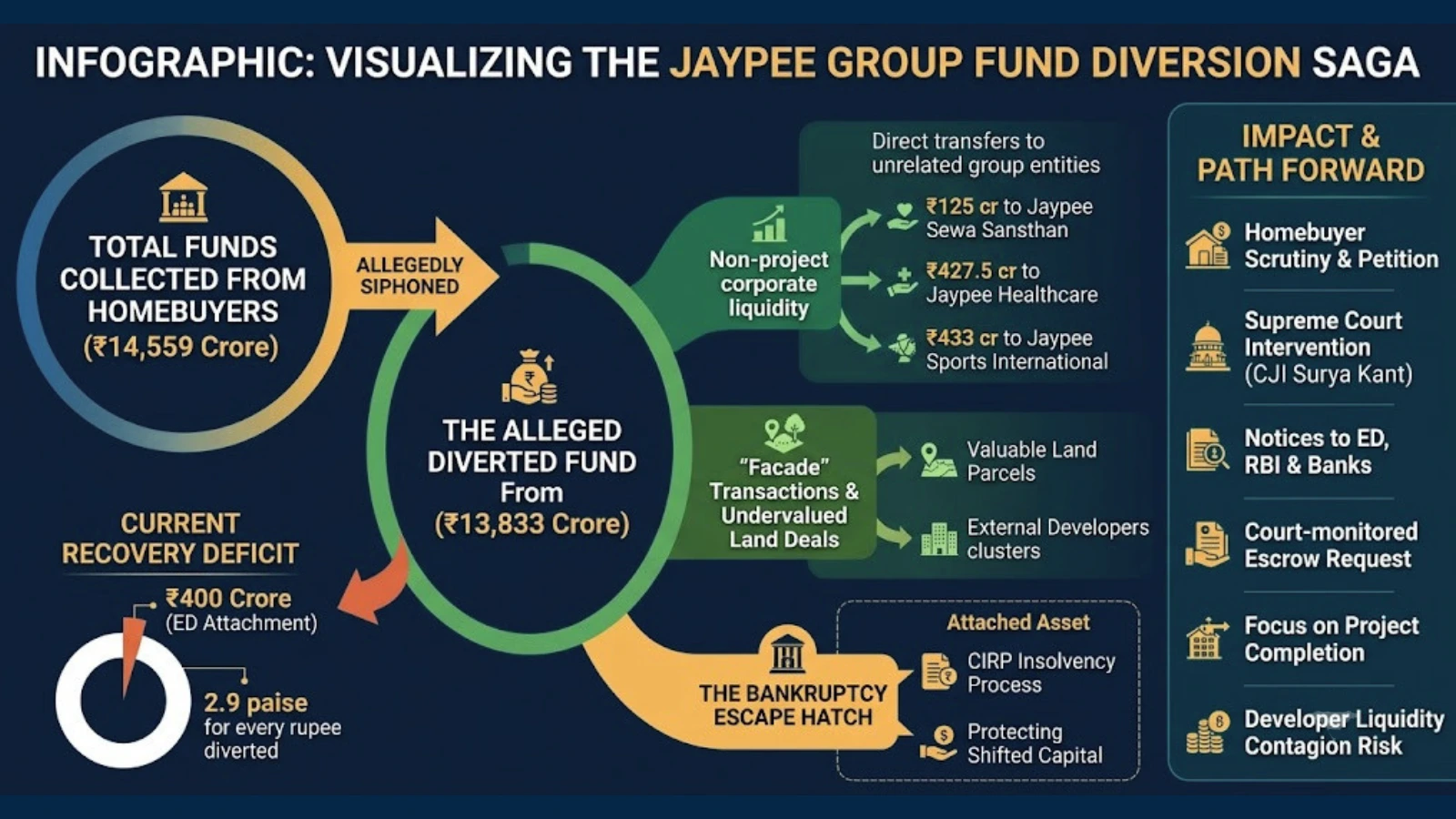

The core mechanics, scale, and current judicial status of the case break down as follows:

The Scale of the Diversion

According to an investigative prosecution complaint by the Enforcement Directorate (ED) and recent writ petitions, by a home buyer, admitted by the Supreme Court of India:

Total Collected: Approximately ₹14,559 crore was collected from over 25,000 homebuyers.

Total Siphoned: An astonishing ₹13,833 crore (roughly 95%) was allegedly diverted away from the construction sites for non-project/corporate liquidity purposes.

The Current Deficit: After years of multi-agency probing, the ED has only provisionally attached about ₹400 crore—which legal representatives point out amounts to just 2.9 paise for every rupee diverted.

The Modus Operandi (How the Money vanished)

The probe reveals that the funds were moved using an intricate network designed to bypass structural accountability and RERA-mandated guidelines:

Direct Group Transfers: Hundreds of crores were transferred straight into unrelated group entities. This included entries like ₹125 crore to Jaypee Sewa Sansthan, ₹427.5 crore to Jaypee Healthcare, and ₹433 crore to Jaypee Sports International.

"Facade" Transactions & Undervalued Land Deals: Jaypee allegedly transferred valuable land parcels and development rights to five primary clusters of external real estate developers. The ED termed these transactions as mere "facades" supported by fictitious credit advices and double sub-lease structures executed primarily to avoid stamp duty and obscure capital trails.

The Bankruptcy Escape Hatch: After stripping the primary entities (JAL and JIL) of capital and assets, the projects were essentially pushed into insolvency under the Corporate Insolvency Resolution Process (CIRP), stalling construction indefinitely while protecting the shifted capital in secondary entities.

Current Legal and Judicial Status

The case has seen sharp escalation with aggressive institutional actions and homebuyer petition:

Executive Arrests: Manoj Gaur, the Executive Chairman of JAL, was arrested by law enforcement in late 2025 and remains in judicial custody over money laundering charges.

Supreme Court Intervention: Led by Chief Justice Surya Kant, a Supreme Court bench issued notices to the Union Government, the ED, and the Reserve Bank of India (RBI), alongside regional authorities (UP RERA, NOIDA, YEIDA). The court has demanded a clear timeline and status report from investigators.

Scrutiny on External Developers: The apex court has also sent notices to several external developer entities who were the beneficiaries of Jaypee’s secondary land and development rights transfers, expanding the risk of transactional contagion across the NCR market.

Restitution Mechanism: Request for a court-monitored escrow account funded by ED attachments to prioritize project completion over other creditor claims.

The involvement of the RBI is particularly telling. The petition seeks an audit of all banks that extended credit to these projects. If the audit reveals that institutional lenders effectively funded "facade" deals, we may see a tightening of credit for mid-to-large scale developers in NCR, potentially impacting the liquidity of ongoing premium launches as well.

Why This Case Matters for Real Estate Investors

The Jaypee saga highlights a critical paradigm shift in how capital health is evaluated in the premium real estate market.

During the growth years of the Yamuna Expressway and Noida’s expansion, these projects were marketed as high-velocity investment assets. However, the current petition highlights a fundamental breakdown in capital discipline.

When retail money is structurally weaponized to fund broader corporate debts rather than physical brick and mortar, the retail investor is left exposed to massive legal gridlocks where exit flexibility completely evaporates.

The ongoing litigation seeks to establish a historic precedent: creating a court-monitored escrow system funded strictly by ED asset attachments to ensure recovered capital goes directly toward project completion rather than satisfying institutional banking debts first.

For an investor too, this underscores the necessity of moving beyond "launch momentum" and looking into the transparency of a developer's capital stack and this is precisely the reason ready-to-move homes are back in consideration of serious investors. At least it gives an upfront confidence that someone can actually live in those apartments instead of seeing paper appreciation.

Despite localized developer distress, the Noida Expressway corridor is witnessing a massive institutional re-rating in 2026. This resilience is anchored by two critical milestones: unprecedented absorption of Grade A office space by reputed firms and DLF’s highly anticipated entry into Sector 108.